Jeffrey LoydUnlock the Value of Your Home: How Installing Solar Increases Your Home’s Sale Price & Attracts…Installing solar panels on your home is a smart investment, not only by saving on energy costs, but also by increasing the overall value of…·2 min read·Jan 11, 2023----

Jeffrey LoydWTF is a 2–1 Buy down?Get the seller to pay part of your mortgage payment for the first two years. That’s a 2–1 buy down.·3 min read·Oct 26, 2022----

Jeffrey LoydWTF is a Seller’s Concession?A seller’s concession (a/k/a seller’s assist or seller’s credit) is a credit to the buyer to cover the cost of the transaction. It can only…·3 min read·Oct 16, 2022----

Jeffrey LoydDoes my solar loan change my Debt To Income (DTI) Ratio?Yes — all loans or lease payments change your debt to income ratio. Let’s talk about how it works.·2 min read·Jun 20, 2022----

Jeffrey LoydWTF is a Closing Protection Letter (CPL)?The Closing Protection Letter protects the lender and/or the buyer — the insured party — if there is misconduct by the closing agent. It’s…·1 min read·Jun 7, 2022----

Jeffrey LoydWTF is per diem interest?Per diem interest is the dollar amount you pay in interest on your mortgage per day.·2 min read·Jun 1, 2022----

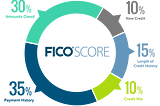

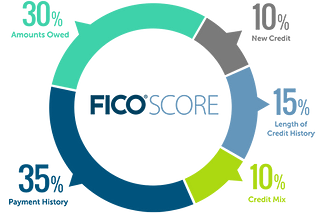

Jeffrey LoydHow do I increase my credit score?While it may not be the answer borrowers want to hear, repairing your credit is the best thing to do before you submit a mortgage…·4 min read·May 26, 2022----

Jeffrey LoydBuying A House With Bad Credit?Buying a home is on everyone’s bucket list. Whether you want to buy a home because you finally want to settle down, or you are tired of…·4 min read·May 16, 2022----

Jeffrey LoydWTF is an Appraisal Management Company (AMC)?“Please reach out to the appraiser and tell them I’ll be late meeting them at the house”·3 min read·May 3, 2022----

Jeffrey LoydWTF is a Mortgage Contingency?A financing contingency (aka mortgage contingency) is a clause in the contract of sale that gives buyers time to apply for and obtain…·2 min read·Mar 18, 2022----